Venture capital funding in the U.S. fell to its lowest level in six years in terms of venture deal value and the lowest level in deal count in three years during the third quarter.

The Venture Monitor report from the National Venture Capital Association showed U.S. VC activity fell to its lowest deal value level since Q2 2018.

“The last 18 months have seen a level of tumult in the economy that would have been unimaginable just a few years earlier, but amid stormy seas, VC remains well positioned to ride the waves,” the report said.

While generative AI exploded this year, geopolitics — not even counting the latest war in Israel and Gaza — inhibited the enthusiasm, with the stock market showing that investors are cautious.

Event

GamesBeat Next 2023

Join the GamesBeat community in San Francisco this October 23-24. You’ll hear from the brightest minds within the gaming industry on latest developments and their take on the future of gaming.

Deal counts are on track to have the lowest year since before the pandemic in 2019. Overall, the market remains under considerable stress, the report said. More companies are taking bridge, continuation, or down rounds; inside rounds are at multiyear highs; and there are fewer rounds with a new lead investor obtaining a board seat than at any time in at least a decade. Investors and founders alike are optimizing for stability and cash flow to meet the challenges of the current market.

However, the ecosystem remains well capitalized, and additional sources of liquidity from federal programs like the Inflation Reduction Act and the CHIPS and Science Act are becoming available.

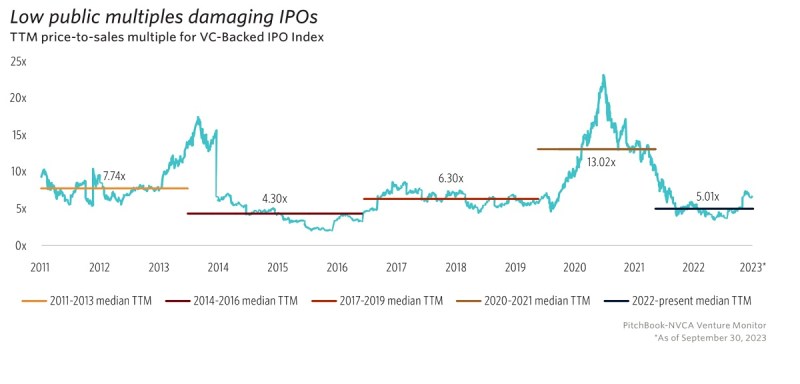

Meanwhile, the stock market’s low multiples in price/sales ratios for public companies are causing IPOs to dry up. Current estimates place the number of companies waiting to go public at 75, and while exit activity is expected to be modest in the near future, the impending listings of household names like Stripe, Chime, and Reddit could portend a more robust liquidity environment.

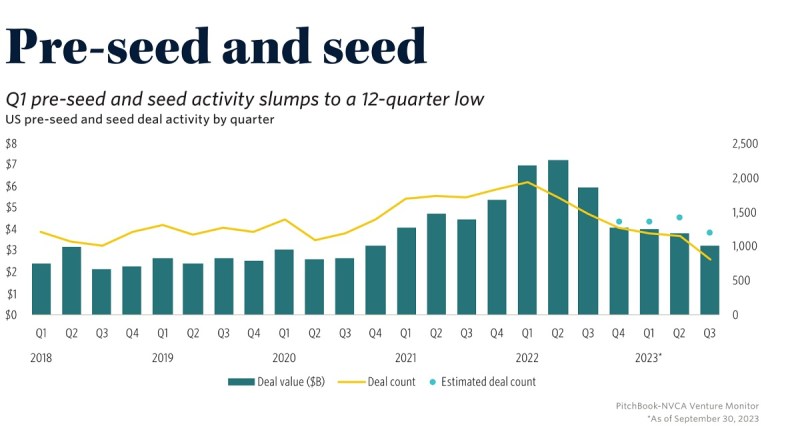

And pre-seed and seed deal counts in the U.S. have hit a 12-quarter low, or the lowest since 2020. On the front end of the market, the relative share of pre-seed to early-stage deals dropped consistently over the

past year.

In comparison, late-stage and venture-growth deals have been on a relatively flat trend over the past

several quarters. There has also been a marked decrease in megadeals over the past year, with deals over $100 million making up 48.5% of deal value in Q3, a far cry from their 60.0% of deal value in Q4 2021.

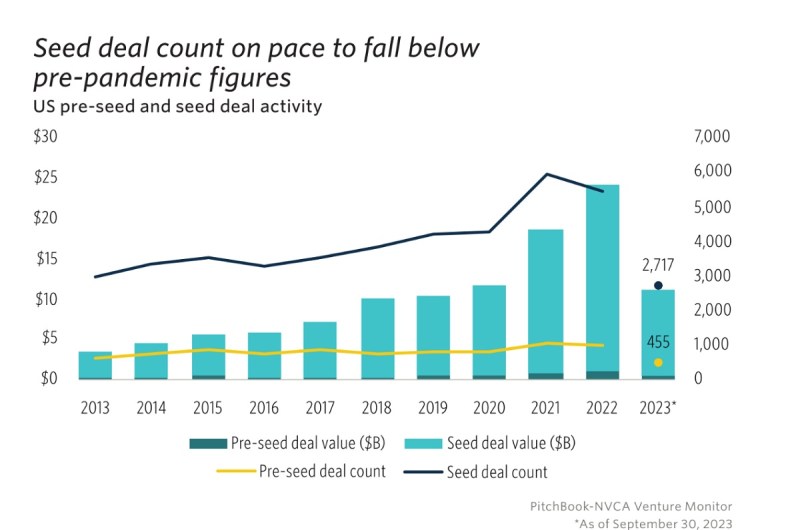

Seed deal counts themselves are on track to fall below pre-pandemic numbers.

Deals are still concentrated in regional hubs across the U.S.

Female founders are finding the market to be particularly difficult.

Q3 exits saw an uptick mainly because of the Instacart and Klaviyo IPOs. Exits via mergers are carrying additional regulatory risks. In July, the Federal Trade Commission (FTC) and Department of Justice (DOJ) laid out new guidelines for approving mergers. The NVCA said it has a number of concerns about the new FTC guidelines, which it said significantly raise the risk of small company acquisitions being blocked for theoretical reasons that have little underpinning in reality and misrepresent nascent firms that fall well short of having monopoly power as being “dominant.”

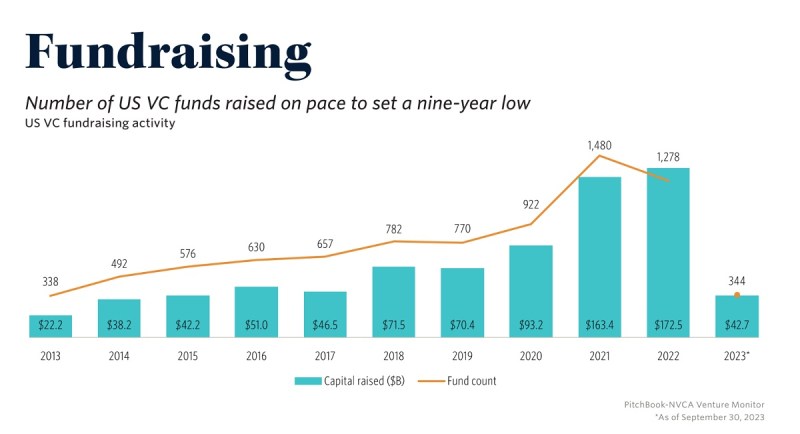

Lastly, fundraising for new VC funds hit a nine-year low. In 2022, fundraising was concentrated in the hands of the largest funds, with nearly half of all capital committed going to funds over $1 billion. The relative share of committed capital to funds valued between $100 million and $1 billion increased sharply over the year, making up nearly two-thirds of funds raised in 2023 so far. Despite the stronger relative performance of mid-cap funds, 2023 has been a difficult year for emerging managers trying to raise first funds, with nearly three out of every four dollars raised in 2023 going to an established manager and first-time funds pacing toward their lowest count in roughly a decade.

In other information, software deals are at a multiyear low, while life sciences investment, while down, is at the highest relative level since 2020.

GamesBeat’s creed when covering the game industry is “where passion meets business.” What does this mean? We want to tell you how the news matters to you — not just as a decision-maker at a game studio, but also as a fan of games. Whether you read our articles, listen to our podcasts, or watch our videos, GamesBeat will help you learn about the industry and enjoy engaging with it. Discover our Briefings.