French startup Indy has recently closed a new funding round of $44 million (€40 million) with BlackFin Capital Partners leading the round. Indy started as an automated accounting platform for freelancers and other self-employed people.

But the company has been slowly iterating on its product to become an all-in-one platform for freelancers, from accounting to company creation, tax preparation, invoicing and (soon) business banking. It’s an interesting example of the positive effects of bundling in a software-as-a-service company. And it could inspire other entrepreneurs addressing a highly fragmented market of potential customers.

As long as you’re running a company without any employee, Indy wants to offer all the administrative and finance tools that you need to run your business. It’s designed for freelancers, self-employed people, doctors, architects, lawyers, etc.

Other investors in the recent funding round include La Maison and iXO. Indy closed its funding round this summer. While the startup didn’t want to share its valuation, the company said that it’s higher than the company’s valuation after its previous €35 million funding round ($38.3 million at today’s exchange rate).

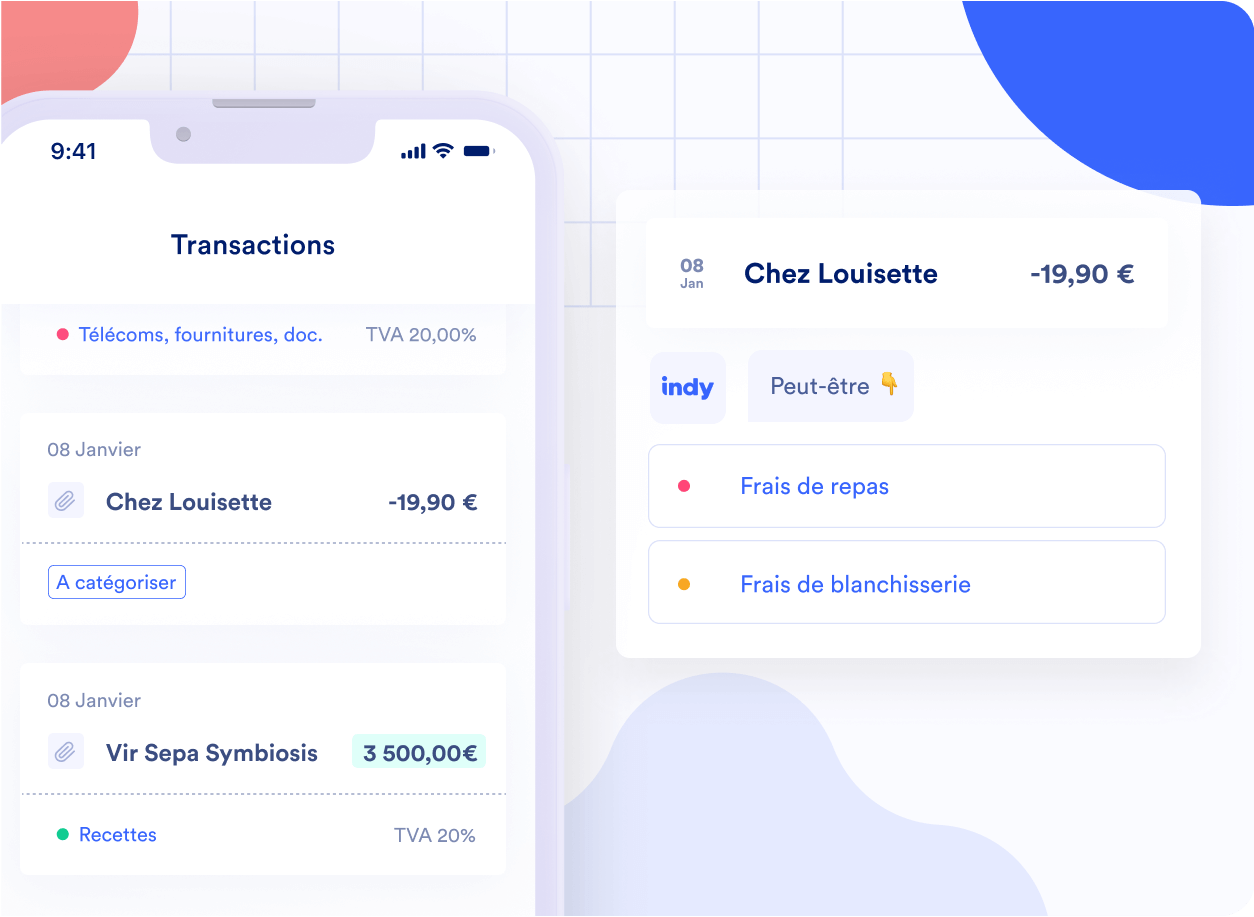

Image Credits: Indy

Indy’s core feature remains its automated accounting feature. When you create an account, you can automatically start synchronizing your bank account with Indy so that past and future transactions are automatically fetched.

After that, Indy tries to categorize each transaction automatically. In some cases, users have to indicate the type of transaction in the app. Customers add a receipt to each transaction — VAT is automatically detected and receipts are then automatically archived and can be used in the event of a tax audit.

At the end of the year, Indy can pre-fill tax forms and send them to the corporate tax administration directly. Similarly, Indy handles VAT returns.

Indy’s accounting tools are free to use forever. As soon as you want to generate tax forms and submit them, you have to pay a monthly subscription. But it remains much cheaper than hiring an accountant.

“As we are on average four to five times cheaper than a chartered accountant for the tax preparation part, there are many people who are using our free services and who will also subscribe to our paid services. But it’s up to them, they can also decide to hire an accountant,” Indy co-founder and CEO Côme Fouques told me.

Product bundling playbook

With this simple product positioning, Indy managed to convince tens of thousands of paid subscribers. But the company hasn’t been standing still as it rolled out other products to turn Indy into a product suite.

For instance, you can now create quotes and invoices from Indy and store them in your user account. Of course, you can always use Word or Excel for these documents, but there are some benefits in having those documents in Indy directly. For instance, when a client pays an invoice with a bank transfer, Indy can automatically mark an invoice as paid.

Similarly, before you can use a product like Indy, you actually need a company to bill customers. In France, even if you’re a part-time freelancer looking for additional income, there is some paperwork involved and there are multiple options.

The startup helps you make the right decisions when you create your company. Unlike traditional company creation services, Indy offers this service for free as long as you start a subscription — but you can cancel that subscription whenever you want.

These products increase the product stickiness and users are more likely to recommend Indy to other self-employed people. Similarly, the sales funnel works particularly well as a good portion of people who want to become freelancers will have to pick a company creation service first.

The next step is clear: Indy is going to become a fintech startup. In just a few months, the startup will offer a free business bank account with a payment card. Once again, it makes sense to bundle this service as current customers have to switch between their banking app and Indy to control their business finances.

Current companies working on business banking, such as Qonto and Shine in France, focus heavily on small and medium companies. They don’t have a basic product offering with basic features that would work well for freelancers. “Business banking for a self-employed person is pretty basic — they want to send money via a transfer, receive money via a transfer, have a payment card, and that’s all there is to it,” Fouques said.

And Indy can then leverage this fintech angle for other services. For instance, the company could offer new payment methods for invoices, such as online card payments, QR code-based payments or using the smartphone as a contactless card reader.

“As we offer all those features in the same service, we make huge economies of scale and we save money on user acquisition costs,” Fouques said. “This means we can offer a whole range of services free of charge — services which would otherwise be paid services somewhere else. At the same time we have a hyper-healthy, hyper-scalable model.”

Some companies have identified the same problem in the U.S., such as Found and Lili — they’ve both raised around $80 million according to Crunchbase data. Indy isn’t going to compete head-to-head with these well-capitalized companies. Instead, the French startup is looking at other European countries to see if it can replicate its service in other markets.

But Indy is still very much focused on its home market as there are millions of self-employed people in France. The market opportunity is already important. And it sounds like Indy has found the right distribution strategy.